The business landscape has shifted fundamentally. Where Michael Porter introduced his five forces framework in 1979, the focus was on linear value chains and physical markets. Today, digital platforms, network effects, and data-driven ecosystems dominate. This guide explores how to adapt Porter’s Five Forces to analyze competitive dynamics in platform businesses. We will examine how traditional barriers to entry and supplier power transform when software, connectivity, and user-generated content become the core assets.

Understanding this adaptation is critical for strategic planning. A static analysis of the past does not reveal the vulnerabilities of a digital ecosystem. By recalibrating the framework, organizations can identify genuine threats and opportunities in a hyper-connected economy.

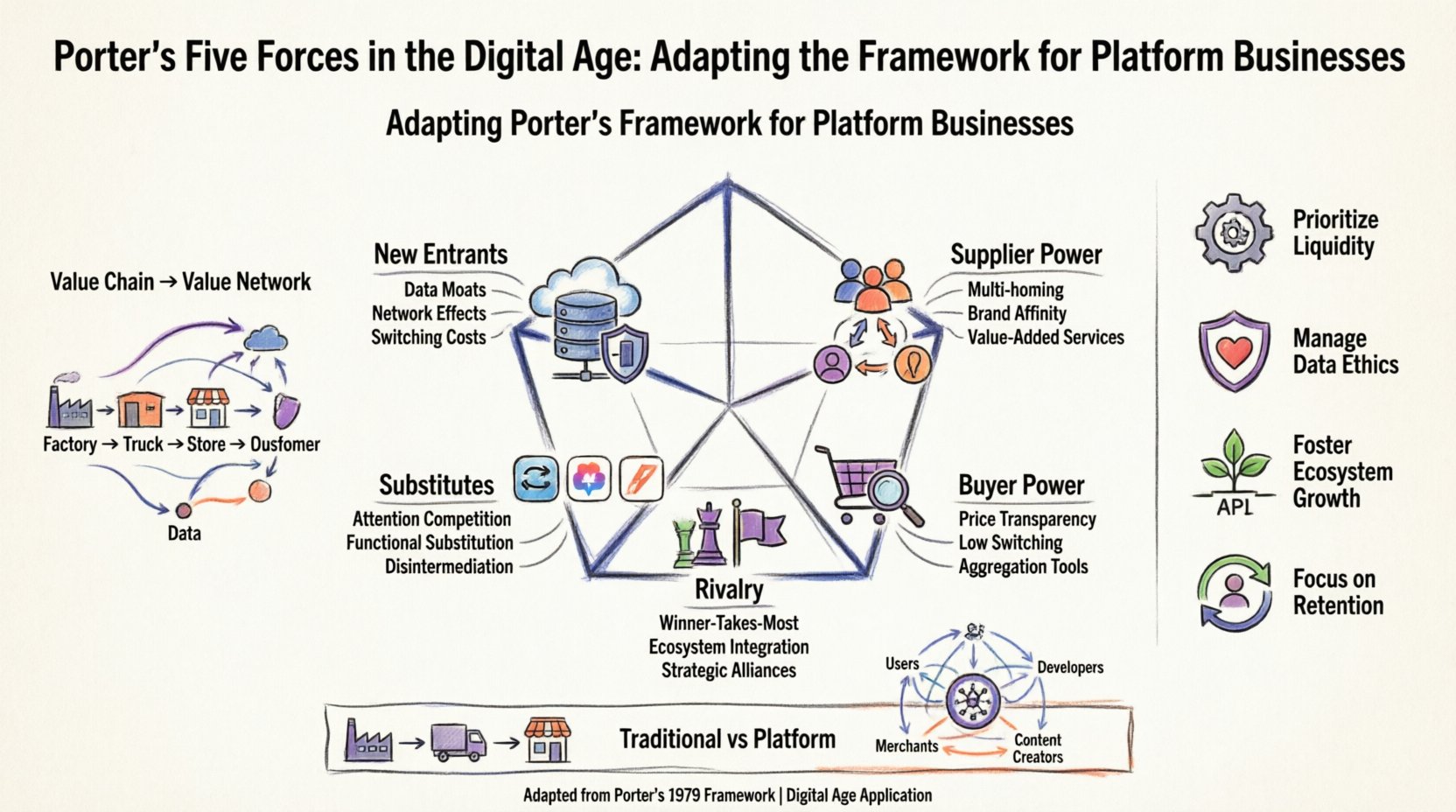

🔄 The Shift from Value Chain to Value Network

In the traditional industrial model, value flows in a straight line: supplier to manufacturer to distributor to consumer. Porter’s framework was designed to assess the power dynamics within this linear flow. However, digital platforms operate as multi-sided markets. They connect distinct groups, such as riders and drivers, or buyers and sellers, facilitating transactions without necessarily owning the inventory.

This structural change alters the definition of competitive boundaries. In a platform context, a competitor might not be another company selling the same product. Instead, it could be a different platform capturing the same user attention or time. The forces interact more dynamically, often reinforcing each other.

- Linear Model: Focuses on cost control and physical distribution.

- Platform Model: Focuses on network effects, liquidity, and data utilization.

- Strategic Implication: The goal shifts from capturing market share to capturing ecosystem share.

When applying the five forces to digital environments, one must consider the role of data. Data acts as both an input for service improvement and a barrier to entry. It is not merely a byproduct of operations; it is a core strategic asset that influences every force.

🚪 Force 1: Threat of New Entrants

In the traditional view, high capital requirements and access to distribution channels act as significant barriers to entry. In the digital age, the barrier to building a functional application has lowered significantly. Cloud infrastructure and open-source libraries allow startups to launch quickly with minimal upfront cost. However, the barrier to achieving scale has increased.

The primary defense for incumbent platforms is the network effect. As more users join, the service becomes more valuable to each individual user. This creates a cycle where new entrants struggle to gain traction because they cannot offer the same utility without the existing user base.

Key Factors Influencing Entry Threats

- Data Moats: Incumbents possess historical data that allows for superior machine learning models or personalized experiences. New entrants start with zero data.

- Switching Costs: Users may face friction when moving data or history to a new platform. This includes learning new interfaces or losing reputation scores.

- Regulatory Hurdles: Compliance with data privacy laws (like GDPR or CCPA) creates significant operational overhead for new market participants.

- API Ecosystems: Incumbents often allow third-party integrations. This creates a dependency where developers build on top of the incumbent, making it harder to leave.

However, new entrants can disrupt by targeting underserved niches. They may offer a better user experience for a specific segment or solve a pain point that the incumbent ignores due to its size. This is often referred to as the “innovator’s dilemma.” A platform focused on the mass market may miss the signals coming from a specialized niche that eventually scales.

👥 Force 2: Bargaining Power of Suppliers

In a platform business, the definition of a “supplier” is often ambiguous. Suppliers are frequently the users themselves. For example, on a ride-sharing platform, the drivers are the suppliers of transportation services. On a content platform, the creators are the suppliers of media.

This relationship creates a unique power dynamic. If suppliers can easily find alternative channels to reach customers, their bargaining power increases. Conversely, if the platform controls the primary traffic flow, suppliers have little leverage.

Supplier Power Dynamics in Platforms

- Concentration: If a few large suppliers dominate the platform, they can demand better commission rates or features.

- Standardization: If the service provided is commoditized (e.g., standard accommodation listings), supplier power is low.

- Multi-homing: Suppliers often operate on multiple platforms simultaneously. If they can serve customers on a competitor’s platform easily, their loyalty to one ecosystem decreases.

- Brand Affinity: If suppliers have strong personal brands, they may be less dependent on the platform’s brand for their revenue.

Platforms mitigate supplier power by providing value-added services. This includes marketing tools, payment processing, insurance, or analytics. By embedding themselves into the operational workflow of the supplier, the platform increases the cost of switching. However, this balance is delicate. If the platform extracts too much value through fees, suppliers may seek to bypass the platform entirely or organize collectively.

💳 Force 3: Bargaining Power of Buyers

Buyers in the digital age have unprecedented access to information. Price transparency is often just a click away. This transparency naturally increases buyer power. However, platform ecosystems introduce complexity. Buyers are not just purchasing a product; they are purchasing access to a network.

The power of buyers is also influenced by the quality of the supply side. If a platform has a vast selection of high-quality suppliers, buyers have more choice and thus more power. If the supply is scarce or exclusive, buyer power diminishes.

Drivers of Buyer Power

- Aggregation Tools: Comparison engines and review aggregators allow buyers to evaluate options instantly.

- Low Switching Costs: Creating an account is often free. Deleting an account is equally easy. This reduces the friction of moving to a competitor.

- Alternative Channels: Buyers can often find similar services through direct websites or other platforms.

- Price Sensitivity: In digital markets, price comparison is frictionless, making buyers highly sensitive to small price differences.

Platforms can counter buyer power by increasing the value of the network. Features like personalized recommendations, loyalty programs, or integrated ecosystems (where one account unlocks multiple services) make it less attractive for buyers to switch. The goal is to move the transaction from a commodity purchase to a relationship-based service.

🔄 Force 4: Threat of Substitutes

In the traditional model, substitutes are often direct alternatives (e.g., tea vs. coffee). In the digital economy, substitutes are often indirect. A platform competing for user time faces competition from any other digital activity. A video streaming service competes with social media, gaming, and news aggregation.

The threat of substitution is high because the cost of trying a substitute is often zero. Users can download a new app and try it without financial commitment. The primary metric for competition is user attention, not just wallet share.

Identifying Substitution Risks

- Functional Substitution: A new technology performs the same function differently (e.g., video calls replacing business travel).

- Attention Substitution: A different digital activity fulfills the same emotional need (e.g., streaming vs. reading a book).

- Disintermediation: Suppliers and buyers may connect directly, bypassing the platform entirely.

- Open Source Alternatives: For software platforms, open-source versions may offer similar functionality without licensing fees.

Platforms must continuously innovate to stay ahead of substitutes. This involves expanding the scope of the service. For instance, a ride-sharing app adding food delivery captures more of the user’s daily needs, making it harder to substitute with a single-purpose competitor.

⚔️ Force 5: Competitive Rivalry Among Existing Competitors

Rivalry in digital markets is often intense. The market is frequently characterized by “winner-takes-all” or “winner-takes-most” dynamics. A slight lead in user base can create a self-reinforcing advantage that makes it nearly impossible for competitors to catch up.

Price wars are common as platforms compete for market share. However, modern competition focuses less on price and more on ecosystem integration. Competitors may not fight on the core product but on the breadth of services surrounding it.

Factors Influencing Rivalry

- Number of Competitors: A crowded market leads to fragmentation and lower margins.

- Industry Growth: In high-growth sectors, companies focus on acquiring users rather than profitability, intensifying rivalry.

- Product Differentiation: Low differentiation leads to price competition. High differentiation allows for premium positioning.

- Exit Barriers: High sunk costs in technology development can trap companies in a market even when profitability is low.

Strategic alliances and partnerships are common tactics to manage rivalry. Instead of fighting for the same users, platforms may integrate with each other to create a broader ecosystem. This shifts the competition from a single platform to a coalition of platforms.

📊 Comparison: Traditional vs. Platform Dynamics

The following table summarizes the key differences in how the five forces manifest in traditional businesses versus platform-based businesses.

| Force | Traditional Business | Platform Business |

|---|---|---|

| New Entrants | High capital requirements for manufacturing and distribution. | Low build cost, high scale cost (network effects). |

| Suppliers | External vendors providing raw materials or components. | Often users (prosumers) providing content or services. |

| Buyers | Price sensitive, limited information access. | Highly informed, multi-homing, attention-based. |

| Substitutes | Direct product alternatives. | Indirect competition for time and attention. |

| Rivalry | Share of market within a specific industry. | Share of ecosystem within a digital lifestyle. |

🧭 Strategic Considerations for Digital Leaders

Applying this adapted framework requires a shift in mindset. Leaders must look beyond immediate financial metrics and consider long-term ecosystem health. The following strategies are essential for navigating the digital competitive landscape.

1. Prioritize Liquidity

Liquidity refers to the ease with which buyers and suppliers can find each other. A platform with high liquidity provides better value than one with high traffic but poor matching. Investment should focus on algorithms and infrastructure that reduce search and transaction time.

2. Manage Data Ethics

Data is the lifeblood of the modern platform, but it is also a liability. Trust is a competitive advantage. How a company handles user data can be a barrier to entry for new competitors or a reason for users to leave. Transparency and ethical data practices should be viewed as strategic assets.

3. Foster Ecosystem Growth

Instead of viewing every interaction as a transaction, view them as opportunities for ecosystem expansion. Encourage third-party developers to build on top of the platform. This increases the value of the platform without increasing the internal operational burden.

4. Focus on Retention Over Acquisition

In a crowded digital market, acquiring a new user is often more expensive than retaining an existing one. Strategies should focus on increasing the lifetime value of users through loyalty programs, superior customer support, and continuous feature updates.

⚠️ Common Implementation Pitfalls

Even with a solid understanding of the forces, organizations often stumble during execution. Recognizing these pitfalls can save resources and prevent strategic missteps.

- Over-reliance on Technology: Technology enables the platform, but it does not guarantee success. Community building and culture are equally important.

- Ignoring Regulatory Trends: Antitrust scrutiny is increasing for dominant platforms. Failing to anticipate regulatory changes can lead to forced divestitures or fines.

- Valuing Growth Over Profitability: While growth is necessary, unsustainable burn rates can lead to failure when capital markets tighten.

- Static Analysis: The digital landscape changes rapidly. A five forces analysis must be updated regularly to reflect new entrants and shifting user behaviors.

🔮 The Future of Competitive Analysis

As digital ecosystems continue to evolve, the lines between industries will blur further. A financial institution might become a marketplace. A logistics company might become a data broker. The five forces framework remains relevant, but its application must be fluid.

Strategic analysis in the digital age is not about predicting a static future. It is about understanding the current state of network effects and data flows to position the organization for resilience. By adapting Porter’s framework to account for platform dynamics, leaders can make more informed decisions about where to invest, where to defend, and where to innovate.

The tools remain the same, but the context has changed. The objective is to build value networks that are robust enough to withstand disruption while flexible enough to capitalize on new opportunities. This requires a deep understanding of the forces at play and the courage to act on that insight.