The healthcare industry operates under a unique set of dynamics that differ significantly from traditional retail or manufacturing sectors. High stakes, complex regulatory frameworks, and a mix of public and private payers create a landscape where strategic positioning is critical. Applying Michael Porter’s Five Forces framework provides a structured method to understand the competitive intensity and profitability potential within this sector. This guide explores how each force manifests in healthcare, focusing on the interplay between market competition and regulatory oversight.

Understanding the Framework in a Clinical Context 🏥

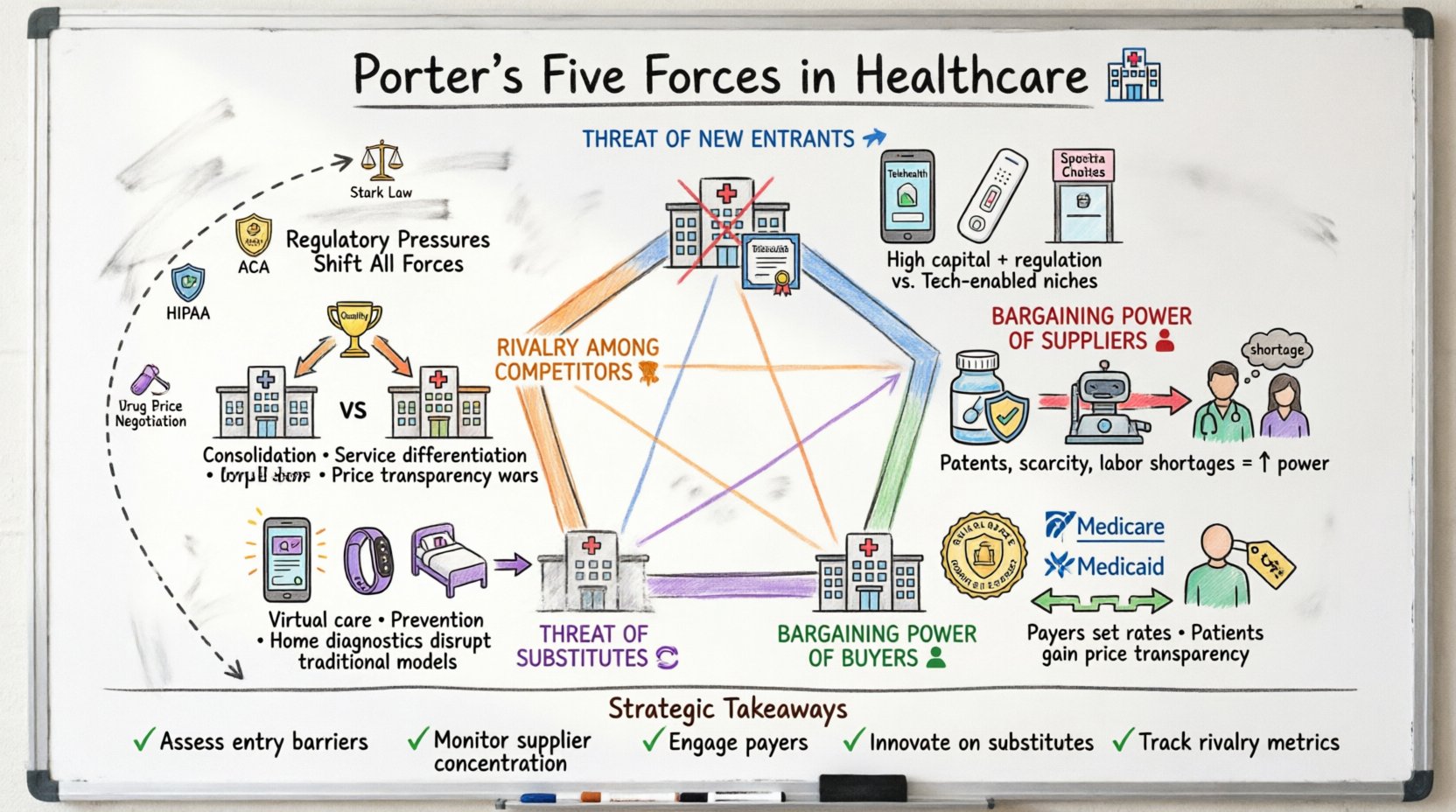

Porter’s Five Forces model evaluates the competitive environment of an industry. In healthcare, these forces are not static; they shift rapidly due to policy changes, technological advancements, and demographic trends. Analyzing these forces helps stakeholders—hospital administrators, pharmaceutical executives, and insurance providers—anticipate challenges and identify opportunities for sustainable growth.

- Threat of New Entrants: How easy is it for new competitors to enter the market?

- Bargaining Power of Suppliers: How much control do providers of essential inputs have?

- Bargaining Power of Buyers: How much influence do patients and payers have on pricing?

- Threat of Substitute Products: Are there alternative solutions to traditional care?

- Rivalry Among Existing Competitors: How intense is the competition between current players?

When applied to healthcare, these categories require a deeper look at specific constraints like the Affordable Care Act, FDA regulations, and Medicare reimbursement rates. The following sections break down each force with specific industry examples.

1. Threat of New Entrants 🚀

Barriers to entry in healthcare are historically high. The capital requirements for building a hospital network are substantial, and licensing for medical professionals involves rigorous training and certification. However, the digital age has lowered some of these hurdles, creating new avenues for competition.

Traditional Barriers

- Capital Intensity: Establishing a physical care facility requires millions in infrastructure investment.

- Regulatory Compliance: Entities must navigate complex laws regarding patient privacy (HIPAA) and safety standards.

- Reimbursement Codes: Gaining access to payment systems like Medicare and Medicaid requires extensive credentialing.

- Brand Trust: Patients often prefer established institutions over unknown providers when facing serious health issues.

Emerging Disruptors

Despite high barriers, new entrants are challenging incumbents by focusing on niche services or leveraging technology.

- Telehealth Platforms: Virtual care startups can operate with minimal overhead compared to brick-and-mortar clinics.

- Direct-to-Consumer Labs: Companies offering home blood tests bypass traditional clinic visits.

- Specialty Clinics: Urgent care and ambulatory surgery centers offer specific services with lower costs.

- Concierge Medicine: High-end private practices cater to patients willing to pay out-of-pocket for access.

The net effect is a mixed picture. While building a hospital remains difficult, entering the market for diagnostic services or remote monitoring is becoming increasingly viable. This forces existing players to innovate or risk losing market share in specific segments.

2. Bargaining Power of Suppliers 💊

Suppliers in healthcare include pharmaceutical companies, medical device manufacturers, and healthcare labor pools. The power dynamics here are heavily influenced by scarcity, patent protection, and labor shortages.

Pharmaceutical and Device Manufacturers

- Patent Protection: Patents grant temporary monopolies, allowing drug makers to set high prices without immediate competition.

- Consolidation: Mergers among device makers reduce the number of options available to hospitals, increasing supplier leverage.

- Specialized Technology: Unique imaging equipment or surgical robots often have few alternatives, locking providers into specific supply chains.

Human Capital

The labor market for healthcare professionals is a critical supply chain. The power of suppliers here relates to the availability of skilled workers.

- Nurse Shortages: High demand for registered nurses gives labor unions and individual providers significant leverage in wage negotiations.

- Specialist Scarcity: Finding board-certified specialists in rural areas is difficult, giving those providers more bargaining power.

- Credentialing: Limited pools of credentialed physicians can restrict the ability of health systems to expand services.

Healthcare providers often respond to supplier power by forming purchasing groups or health system alliances to negotiate better rates collectively. However, when specific drugs or technologies are essential for life-saving procedures, the ability to negotiate is limited.

3. Bargaining Power of Buyers 👥

Buyers in healthcare are complex. They include individual patients, insurance payers, and government agencies. Their power varies depending on the service and the payer structure.

Insurance Payers

Private insurance companies and government programs like Medicare and Medicaid act as the primary buyers of hospital and physician services.

- Network Negotiations: Large insurers can threaten to exclude a hospital from their network, which would drastically reduce patient volume.

- Rate Cap: Government payers often set reimbursement rates based on fixed formulas, limiting the revenue providers can earn.

- Administrative Burden: Payers dictate coding and documentation requirements, adding operational costs to providers.

Patients and Consumers

The rise of high-deductible health plans has shifted more cost burden to patients, increasing their price sensitivity.

- Price Transparency: Regulations requiring providers to publish standard charges allow patients to compare costs more effectively.

- Out-of-Network Options: Patients can sometimes choose out-of-network providers if they can afford the difference, though this is often restricted.

- Advocacy: Patient advocacy groups influence policy, pushing for lower drug prices and better coverage.

While patients rarely have direct control over the prices charged by hospitals, the aggregate power of payers significantly dictates the financial health of healthcare organizations. Providers must balance the need for revenue with the pressure to maintain network contracts.

4. Threat of Substitute Products or Services 🔄

Substitutes are services that fulfill the same need as the primary product but through a different mechanism. In healthcare, these substitutes often come from technology or shifts in consumer behavior.

Telemedicine and Remote Care

Virtual visits can replace many in-person consultations for non-urgent conditions.

- Convenience: Patients prefer the ease of seeing a doctor from home for minor ailments.

- Cost: Virtual visits are often cheaper than office visits, appealing to price-sensitive consumers.

- Chronic Disease Management: Remote monitoring devices allow for ongoing care without frequent hospital trips.

Preventative and Lifestyle Interventions

Preventing illness reduces the need for treatment, acting as a substitute for acute care.

- Wellness Apps: Digital tools for diet and exercise can reduce the incidence of obesity-related conditions.

- Alternative Medicine: Integrative approaches like acupuncture or chiropractic care are often sought for pain management.

- Home Health: Skilled nursing at home can substitute for short-term inpatient hospital stays.

As technology improves, the line between substitute and traditional care blurs. For example, home diagnostic kits are replacing lab visits. This forces traditional providers to integrate these services or risk obsolescence in specific areas.

5. Rivalry Among Existing Competitors 🥊

Competition in healthcare is fierce, particularly in urban markets where multiple hospital systems vie for the same patients and insurance contracts.

Market Consolidation

- Hospital Mergers: Systems merge to gain scale and bargaining power against insurers.

- Acquisition of Physician Practices: Health systems buy independent practices to control the patient referral funnel.

- Vertical Integration: Insurers acquiring provider networks to control the entire care continuum.

Service Differentiation

When price is regulated or opaque, competition shifts to quality and convenience.

- Outcome Data: Hospitals compete on success rates for surgeries and patient satisfaction scores.

- Technology Adoption: Offering the latest robotic surgery or AI diagnostics attracts patients.

- Amenities: Private rooms and concierge services differentiate luxury care options.

Price transparency laws have begun to make competition more visible. Providers are now more aware of how their costs compare to neighbors, which can lead to price wars in self-pay sectors like elective procedures.

Regulatory Pressures as a Strategic Factor 📜

Regulation is not just a compliance requirement; it is a strategic variable that shifts the Five Forces. Understanding how laws impact competition is essential for long-term planning.

| Regulation | Impact on Force | Strategic Implication |

|---|---|---|

| HIPAA | Increases cost of entry | Protects data, creates trust barrier |

| ACA (Affordable Care Act) | Increases buyer power | Expands insurance coverage, shifts cost to providers |

| Stark Law | Limits provider consolidation | Restricts self-referrals, affects mergers |

| Drug Price Negotiation | Reduces supplier power | Forces pharma to innovate or lower prices |

| Reimbursement Models | Shifts focus to value | Pays for outcomes, not volume |

Regulatory bodies like the Department of Justice and the Federal Trade Commission also monitor healthcare mergers closely. A deal that might be approved in retail could be blocked in healthcare due to concerns about reduced competition and higher prices for patients.

Strategic Implications for Stakeholders 🧭

Applying this analysis leads to actionable strategies for different types of organizations within the ecosystem.

For Hospital Systems

- Expand Ambulatory Services: Move services out of the hospital to reduce costs and compete with urgent care.

- Secure Exclusive Contracts: Negotiate with insurers to become the preferred provider in a region.

- Invest in Data: Use analytics to predict patient needs and manage costs effectively.

For Pharmaceutical Companies

- Differentiate via Outcomes: Prove that drugs improve patient health better than competitors.

- Direct Patient Engagement: Educate patients to create demand for specific treatments.

- Adapt to Value-Based Care: Align pricing models with the value delivered to payers.

For Digital Health Startups

- Focus on Interoperability: Ensure your tools work with existing hospital systems.

- Navigate Reimbursement: Understand which services can be billed to insurance.

- Partner with Incumbents: Collaborate with hospitals rather than trying to replace them immediately.

The Future of Competitive Analysis in Healthcare 🔮

The healthcare landscape is evolving toward value-based care, where payment is tied to patient outcomes rather than the volume of services provided. This shift fundamentally alters the Five Forces.

- Collaboration over Competition: Providers are increasingly partnering to manage population health risks.

- Technology Integration: Artificial intelligence and machine learning will reduce costs and improve diagnostic accuracy.

- Patient-Centricity: The patient becomes a more informed consumer, increasing their power.

Strategic planning must account for these shifts. Static analysis is insufficient. Continuous monitoring of regulatory changes and market trends is required to maintain a competitive edge.

Key Takeaways for Strategic Planning 📝

- Assess Entry Barriers: Determine if the market is open to new disruptors or protected by regulation.

- Monitor Supplier Concentration: Diversify supply chains to reduce dependency on single vendors.

- Engage with Payers: Build strong relationships with insurance networks to ensure access.

- Innovate on Substitutes: Develop alternative care models to capture market share.

- Track Rivalry Metrics: Keep an eye on competitor pricing, capacity, and service offerings.

By systematically analyzing these forces, healthcare organizations can make informed decisions that enhance resilience and profitability. The complexity of the industry demands a rigorous approach to strategy, ensuring that every move aligns with both market realities and regulatory requirements.