Building a robust financial platform requires more than just coding skills; it demands a structural approach that ensures data integrity, security, and scalability. Object-Oriented Analysis and Design (OOAD) provides the architectural backbone for complex systems like banking applications. By leveraging core principles such as encapsulation, inheritance, polymorphism, and abstraction, developers can create modular, maintainable, and secure software solutions. This guide explores the practical application of OOP principles in designing a comprehensive banking system.

1. Understanding the Requirements 📋

Before writing a single line of code, the analysis phase identifies what the system must do. A banking system handles sensitive data and financial transactions, making precision critical. The functional requirements define the actions users can perform, while non-functional requirements dictate performance and security standards.

- Functional Requirements:

- Account creation and management (Opening, Closing, Freezing).

- Financial transactions (Deposits, Withdrawals, Transfers).

- Interest calculation and crediting.

- Loan application and repayment processing.

- Generating statements and transaction history.

- Non-Functional Requirements:

- High availability (99.9% uptime).

- Data consistency and ACID compliance.

- Security protocols (Encryption, Authentication).

- Response time under load.

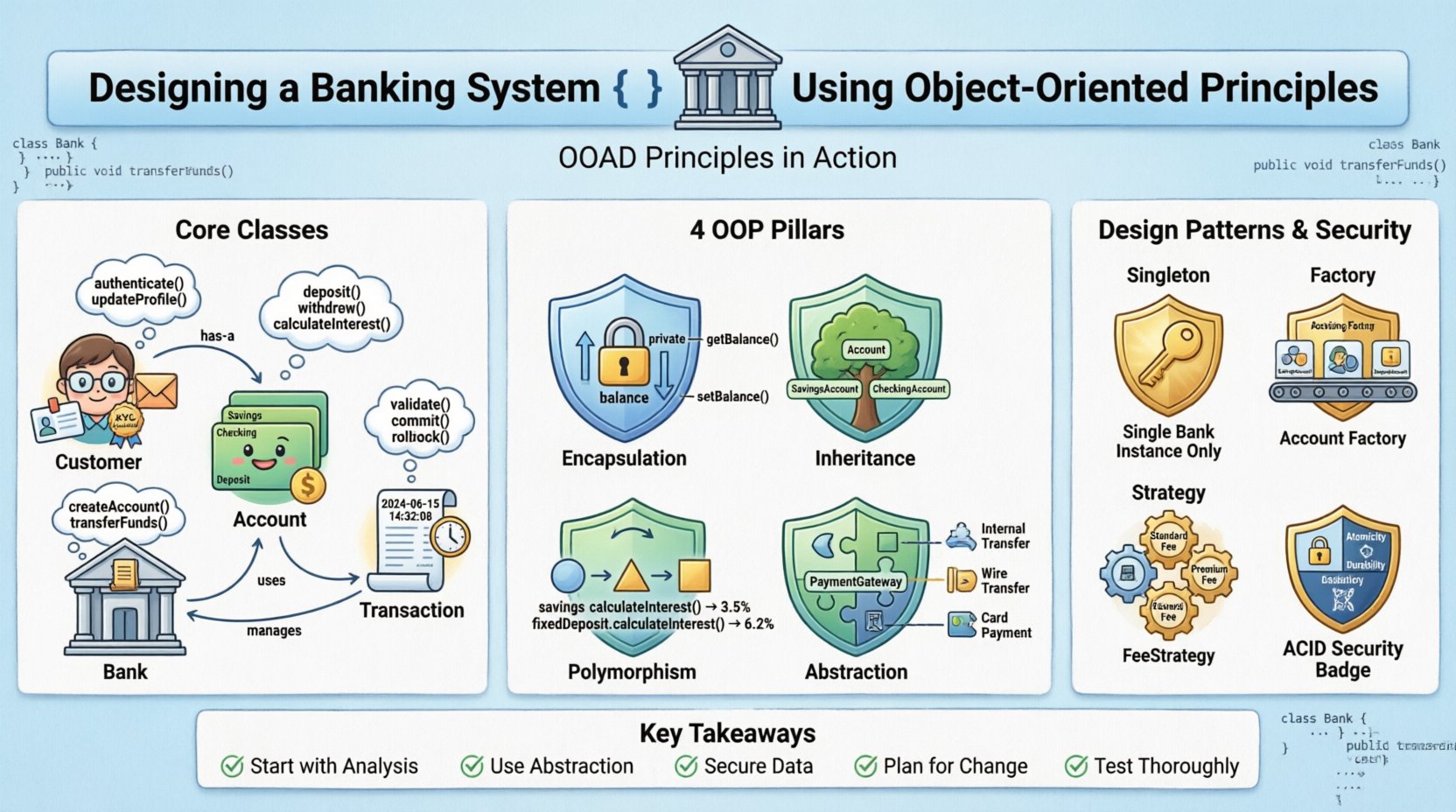

2. Identifying Core Classes and Objects 🧱

The first step in design is identifying the nouns in the requirements. These nouns translate into classes. In a banking context, the primary entities include Customers, Accounts, Transactions, and the Bank itself. Each class represents a specific concept with defined attributes and behaviors.

2.1 The Customer Class

This class represents the individual or entity owning the accounts. It holds personal identification details and contact information.

- Attributes: Customer ID, Name, Address, Contact Number, Email, Kyc Status.

- Behaviors: UpdateProfile, RequestStatement, Authenticate.

2.2 The Account Class

Accounts hold the funds. They are linked to customers and define the type of financial product (Savings, Checking, Fixed Deposit).

- Attributes: Account Number, Account Type, Balance, Interest Rate, Status.

- Behaviors: Deposit, Withdraw, CalculateInterest, Freeze.

2.3 The Transaction Class

This class records every movement of money. It acts as a log entry to ensure an audit trail exists.

- Attributes: Transaction ID, Type (Debit/Credit), Amount, Timestamp, SourceAccount, DestinationAccount.

- Behaviors: Validate, Commit, Rollback.

2.4 Class Attributes Comparison Table 📊

| Class Name | Key Attributes | Primary Methods |

|---|---|---|

| Customer | id, name, email, kycStatus | authenticate, updateProfile |

| Account | accountNumber, balance, type, interestRate | deposit, withdraw, calculateInterest |

| Transaction | txnId, amount, date, type | validate, commit |

| Bank | bankName, branchLocation, totalAccounts | createAccount, transferFunds |

3. Applying Object-Oriented Principles 💎

The strength of this design lies in how it adheres to the four pillars of Object-Oriented Programming. Each principle addresses specific challenges inherent in financial systems.

3.1 Encapsulation 🔒

Encapsulation bundles data and methods together while restricting direct access to some of an object’s components. In banking, exposing balance details publicly is a security risk. Encapsulation ensures that only authorized methods can modify the balance.

- Private Members: The

balancevariable should be private. External classes cannot change it directly. - Public Getters/Setters: A

getBalance()method allows reading the value, while aupdateBalance()method only accepts valid changes through the deposit or withdrawal logic. - Security Benefit: Prevents unauthorized modification of financial records from outside the class scope.

3.2 Inheritance 🌳

Inheritance allows a new class to derive properties and behavior from an existing class. This reduces code redundancy and promotes reusability. Different account types share common features but have specific rules.

- Base Class:

Accountcontains common attributes likeaccountNumberandbalance. - Subclasses:

SavingsAccountandCheckingAccountinherit fromAccount. - Specialization:

SavingsAccountmight add aninterestRateattribute, whileCheckingAccountmight add atransactionLimitattribute.

3.3 Polymorphism 🔄

Polymorphism allows objects to be treated as instances of their parent class rather than their actual class. This is crucial when handling different account types uniformly or applying different calculation logic.

- Method Overloading: A method named

calculateInterestcan accept different parameters (e.g., time period vs. rate). - Method Overriding: The

calculateInterestmethod behaves differently for Savings vs. Fixed Deposits. The system calls the specific implementation based on the object type at runtime. - Benefit: The main system logic doesn’t need to know the specific account type to trigger a calculation; it just calls the method on the parent reference.

3.4 Abstraction 🧩

Abstraction hides complex implementation details and shows only the necessary features of the object. This simplifies the interaction between the user interface and the backend logic.

- Interfaces: Define a

PaymentGatewayinterface with aprocessPaymentmethod. - Implementation: Different payment providers (Internal Transfer, External Wire, Card) implement this interface differently.

- Benefit: If the bank switches payment providers, the core system logic remains unchanged; only the implementation class changes.

4. Design Patterns for Financial Logic 🛠️

Beyond basic principles, specific design patterns solve recurring problems in banking architecture.

4.1 Singleton Pattern 🕵️

The Bank instance should be unique. There should only be one central authority managing the ledger. The Singleton pattern ensures only one instance of the Bank class exists throughout the application lifecycle.

- Use Case: Global configuration management or the central ledger service.

- Constraint: Ensure thread safety to prevent race conditions during concurrent access.

4.2 Factory Pattern 🏭

Creating objects can be complex. The Factory method creates objects without specifying the exact class. This is useful when creating new account types.

- Scenario: A user selects “Savings” or “Current” during account opening.

- Logic: A factory class inspects the request and returns the appropriate Account subclass instance.

- Benefit: The client code remains decoupled from the concrete classes.

4.3 Strategy Pattern 🧭

Algorithms for fee calculation or interest rates vary. The Strategy pattern defines a family of algorithms, encapsulates each one, and makes them interchangeable.

- Example: Different branches might have different fee structures.

- Implementation: A

FeeStrategyinterface is implemented byStandardFeeStrategy,PremiumFeeStrategy, etc. - Benefit: Changing the fee policy does not require modifying the core transaction class.

5. Transaction Management and Security 🛡️

Financial systems must guarantee that money is never lost or duplicated. This requires rigorous transaction management and security measures.

5.1 ACID Properties

Transactions must adhere to Atomicity, Consistency, Isolation, and Durability.

- Atomicity: A transfer involves two steps: debit source, credit destination. Both must succeed, or both must fail.

- Consistency: The database must remain in a valid state before and after the transaction.

- Isolation: Concurrent transactions should not interfere with each other (e.g., two users trying to withdraw the same balance simultaneously).

- Durability: Once committed, the change must survive system failures.

5.2 Security Measures

Protecting data is paramount. Encryption and authentication are non-negotiable.

- Data Encryption: Sensitive fields like account numbers and personal details must be encrypted at rest and in transit.

- Authentication: Multi-factor authentication (MFA) should be enforced for high-value transactions.

- Logging: Every action must be logged in an immutable audit trail. This helps in forensic analysis if a breach occurs.

- Validation: Input validation prevents injection attacks. All user inputs must be sanitized before processing.

6. Handling Edge Cases and Errors ⚠️

Robust systems anticipate failure. The design must handle scenarios that fall outside normal usage.

6.1 Insufficient Funds

The withdrawal method must check the balance before processing. If the balance is insufficient, the system must throw a specific exception or return an error state, preventing negative balances unless overdraft protection is active.

6.2 Concurrent Access

Locking mechanisms (e.g., Optimistic or Pessimistic Locking) prevent two transactions from modifying the same account simultaneously. This avoids race conditions where the balance might be read twice before being updated.

6.3 Network Failures

If a network error occurs during a transfer, the system must ensure the transaction is rolled back. The client should be notified of the failure, and the funds should remain in the source account.

7. Testing and Validation 🧪

Before deployment, the system undergoes rigorous testing to ensure reliability.

- Unit Testing: Test individual classes (e.g.,

Account.calculateInterest) in isolation to verify logic. - Integration Testing: Verify how the Account class interacts with the Transaction and Database layers.

- Load Testing: Simulate peak traffic (e.g., end-of-month salary credits) to ensure the system handles concurrent requests without crashing.

- Security Testing: Perform penetration testing to identify vulnerabilities in authentication and data handling.

8. Maintenance and Scalability 🔧

The software lifecycle does not end at launch. The object-oriented structure facilitates future changes.

- Modularity: If a new account type is needed, developers can create a new subclass without altering existing code.

- Refactoring: As requirements change, internal methods can be optimized without affecting external interfaces.

- Scalability: The separation of concerns allows horizontal scaling of specific services (e.g., the Transaction service can be scaled independently from the User Profile service).

9. Summary of Design Decisions 📝

The following table summarizes the mapping between banking requirements and the OOAD solution.

| Requirement | OOAD Solution | Benefit |

|---|---|---|

| Secure Data Access | Encapsulation | Prevents unauthorized balance modification |

| Different Account Types | Inheritance | Reduces code duplication |

| Variable Interest Logic | Polymorphism | Flexible calculation strategies |

| Multiple Payment Methods | Abstraction | Easy integration of new payment gateways |

| Central Ledger | Singleton Pattern | Ensures single source of truth |

10. Future Considerations 🚀

As technology evolves, the banking system must adapt. Modern trends include real-time processing, blockchain integration, and AI-driven fraud detection. The object-oriented foundation remains relevant because it allows these new components to be integrated as new classes or strategies without disrupting the core architecture.

For instance, integrating a blockchain ledger would involve creating a new BlockchainLedger class that implements the existing Ledger interface. The rest of the system remains unaware of the change. This modularity is the primary advantage of the OOAD approach in financial software development.

11. Key Takeaways for Developers 👨💻

- Start with Analysis: Understand the business rules before designing classes.

- Use Abstraction: Hide complexity behind clean interfaces.

- Secure Data: Never expose sensitive variables publicly.

- Plan for Change: Use design patterns to accommodate future requirements.

- Test Thoroughly: Financial errors are costly; validation is key.

Designing a banking system is a complex task that requires careful planning and adherence to best practices. By applying Object-Oriented Analysis and Design principles, developers can create systems that are not only functional today but are also adaptable for the future. This structured approach ensures that the software remains secure, maintainable, and efficient throughout its lifecycle.